The EHES blog Positive Check has moved and can be found on the EHES website:

https://ehes.org/category/blog/

The EHES blog Positive Check has moved and can be found on the EHES website:

https://ehes.org/category/blog/

by Vinzent Ostermeyer, Lund University, Department of Economic History.

Read more about Vinzent's reserach here.

Read the full paper (open access) here.

A common

periodization of economic development is that first labor shifts out of

agriculture into industry and only then the service sector grows. However, such

views disregard that already during the late 19th century

— a period commonly associated with rapid industrialization — services were an

important part of the economy growing at rates comparable to or even faster

than industry (Weiss, 1967, 1971; Hartwell, 1973; Gemmell and Wardley, 1990;

Broadberry et al., 2010, 2018; Rosés and Wolf, 2019). Why did such a service

economy evolve earlier than conventionally thought?

While

economic historians traditionally focus on explaining the emergence of

industry, less work has been devoted to studying the emergence of services

(Broadberry et al., 2018). Given that the historic origins of the service

sector are largely unclear, it can be useful to look at contemporary periods

for possible explanations. The employment multiplier framework formulated by

Moretti (2010) predicts that industrial growth should have been a key

contributor to the growth of services as each new industrial jobs stimulates

through increased demand the local service sector. Moretti (2010) shows that in

the contemporary USA 1.6 service jobs are created for each new industrial job.

This number increases to 2.5 for the creation of skilled industrial employment.

The multiplier is larger for skilled industrial jobs because they require

higher levels of human capital, which translates into higher productivity and

wages. Additionally, relatively wealthier households tend to spend more of

their income on services.

I

contribute to the literature on the historical emergence of services by testing

whether and if so by how much multiplier effects can explain the emergence of

the service sector. Specifically, I use full-count census data across a set of

countries to estimate employment multipliers in a consistent way for the late

19th century.

Using data from the IPUMS project published by the Minnesota Population Center

(2019) and Ruggles et al. (2021), I build a detailed panel measuring the size

of the industrial and service sectors at the regional level in the USA, Great

Britain, and Sweden. In my approach, I classify the occupation, sector, and

skill levels of individuals according to HISCO and HISCLASS codes.

I then follow the regression approach by Moretti (2010). For each country, I regress the change in the number of jobs (E) in the non-tradable (NT) – i.e., service – sector on the change in log total employment in the tradable (T) – i.e., industrial – sector for region r between two census years t. This approach controls for the potential bias of time-invariant factors and common shocks across regions in a given year. I use cluster-robust standard errors at the regional level in all regressions to account for serial correlation and possible heteroscedasticity in the standard errors.

β1 measures the employment multiplier as an elasticity. To give it a more intuitive interpretation, I multiply it with the ratio of non-tradable to tradable jobs. The employment multiplier then measures the number of jobs created in the non-tradable sector given an additional job in the tradable sector. To also isolate arguably exogenous variation in the demand for labor in the tradable sector, I follow Moretti (2010) by using a Bartik shift-share instrumental variables approach where I instrument the change in tradable employment with a region-specific weighted average of the national growth in tradable employment. Intuitively, the instrument relies on the notion that cities with a higher initial share of tradable employment in industry i should experience a larger positive shock if this industry grows at the national level.

My

main finding is that across countries, the addition of one tradable job in a

local labor market led to the creation of 0.5 to 1 additional non-tradable

job(s). Next, I divide tradable employment into a skilled and non-skilled part

and use both as outcome variable. As predicted, I find that the multiplier

effect is entirely driven by the creation of skilled tradable employment. The

effect was largest in the USA where adding one skilled tradable job increased

local service employment by about 2.5 jobs. In Great Britain and Sweden a

little less than one service job was created.

One

concern against utilizing multiplier effects for public policy is that they

could mainly lead to the expansion of unskilled service employment. I argue

that such concerns are unwarranted for the late 19th century.

By splitting the service sector into a skilled and non-skilled part and

estimating separate multiplier effects for both, I show that multiplier effects

contributed to the growth of both types of services. I also show that employment multiplier effects

increased employment across a range of different services and most notably

personal and business services. Especially the multiplier effect for business

services is noteworthy as they were key for industrialization and required

relatively more skills.

This

paper has several contributions to and implications for the literature. In a

comparison to a step-wise understanding of economic development where

industrialization occurs first and only afterwards there is an emergence of

services, I show that both sectors are intimately related as a substantial part

in the growth of services is due to simultaneous industrial growth. Because the

industrialization during the late 19th century created growth in

other sectors as well, its role for economic development is arguably broader

than often recognized.

My paper

also contributes to the current literature on employment multipliers. While

this literature focuses on single countries in contemporary settings (Moretti,

2010; Moretti and Thulin, 2013), I employ a unified methodology and use for the

first time data harmonized across a set of countries. This enables a plethora

of comparisons. Given that I follow Moretti (2010), I can compare the historic

multiplier effects in the USA to the contemporary ones. Overall, both

multipliers are of very similar size. Second, I can compare the employment

multiplier effects across countries historically. Consistent with the

theoretical framework, I find larger multiplier effects in countries that are

less technologically advanced and have a higher geographic internal mobility, e.g.,

Sweden compared to Great Britain.

References:

Broadberry, S., Federico, G., and Klein, A.

(2010). Sectoral developments, 1870–1914. In Broadberry, S. and O’Rourke, K.

H., editors, The Cambridge Economic History of Modern Europe, pages 59–83. Cambridge University

Press, Cambridge.

Broadberry, S. N., Cain, L. P., and Weiss, T.

(2018). Services in American Economic History. In Cain, L. P., Fishback, P. V.,

and Rhode, P. W., editors, The Oxford Handbook of American Economic History, Vol. 1, pages 234–260. Oxford University

Press, Oxford.

Crouzet,

F. (1982). The Victorian Economy. Methuen, London.

Gallman, R. E. and Weiss, T. J. (1969). The

Service Industries in the Nineteenth Century. In Fuchs, V. R., editor, Production and

Productivity in the Service Industries, pages 287–381. NBER, Cambridge, Massachusetts.

Gemmell, N. and Wardley, P. (1990). The

contribution of services to British economic growth, 1856–1913. Explorations in Economic

History,

27(3):299–321.

Hartwell, R. M. (1973). The Service Revolution:

The Growth of Services in Modern Economy. In Cipolla, C. M., editor, The Fontana Economic

History of Europe,

number 3 in The Industrial Revolution, pages 358–396. Wiliam Collins Sons &

Co. Ltd, Glasgow.

Klein, A. (2019). Regional inequality in the

United States: Long-term patterns, 18802010. In Rosés, J. R. and Wolf, N.,

editors, The Economic Development of Europe’s Regions: A Quantitative History

since 1900, pages

363–386. Routledge, New York.

Lee, C. H. (1979). British Regional Employment Statistics 1841-1971. Cambridge University Press,

Cambridge.

Lee, C. H. (1984). The service sector, regional

specialization, and economic growth in the Victorian economy. Journal of Historical

Geography,

10(2):139–155.

Mathias, P. (1969). The First Industrial Nation: An Economic History of Britain, 17001914. University Paperbacks. Butler

& Tanner Ltd., London.

Moretti,

E. (2010). Local Multipliers. American Economic Review, 100(2):373–377.

Moretti, E. and Thulin, P. (2013). Local

multipliers and human capital in the United States and Sweden. Industrial and Corporate

Change,

22(1):339–362.

Minnesota Population Center (2019). Integrated

Public Use Microdata Series, International: Version 7.2 [dataset], Minneapolis,

MN, IPUMS, 2019. https://doi.org/10.18128/D020.V7.2.

Rosés, J. R. and Wolf, N. (2019). Regional

economic development in Europe, 1900-2010. In Rosés, J. R. and Wolf, N.,

editors, The Economic Development of Europe’s Regions, Routledge Explorations in Economic History,

pages 3–41. Routledge, New York.

Ruggles, S., Flood, S., Foster, S., Goeken, R.,

Pacas, J., Schouweiler, M., and Sobek, M. (2021). IPUMS USA: Version

11.0 [dataset]. Minneapolis, MN. https://doi.org/10.18128/D010.V11.0.

Schön, L. (2010). Sweden’s Road to Modernity: An Economic History. Studentlitteratur, Lund.

TombstoneWeb.com (2011). Tombstone Arizona

History. https://web.archive.org/web

/20110625071235/http://www.tombstoneweb.com/history.html.

Weiss, T. (1967). The Service Sector in the

United States, 1839 to 1899. The Journal of Economic History, 27(4):625–628.

Weiss, T. (1971). Urbanization and the growth

of the service workforce. Explorations in Economic History, 8(3):241–258.

Jan Luiten van Zanden and Emanuele Felice

The full paper can be read here

How wealthy, and how unequal, was pre-industrial Europe? And how rich

was the South of Europe compared to the North Sea area: did the Little

Divergence already start in the late Medieval Period? And if this was the case,

what are the reasons for the decline, perhaps starting already in the XV

century, of Italy?

These are the main questions we address in this reconstruction of the

historical national accounts of Tuscany in 1427. It is based on one of the most

detailed, extensive and probably reliable quantitative source available for

Medieval Europe, the Florentine Catasto of 1427, which has accurate information

on the composition, the occupations and assets of 61,123 households in Tuscany

in that year.

According to our estimates, by the early XV century Tuscany was in per

capita GDP, in real terms, only slightly above England (maybe less than 20%),

and slightly less above Holland (maybe around 13%); this gap is much smaller

than the one resulting from the Maddison project (in 1427 Centre-North Italy

has a GDP per capita between 70 and 100% higher than Holland and England, in

the same period).

In addition, in the process of creating a benchmark estimate of

Tuscany’s GDP in 1427, we also learn a lot about the structure of its economy.

In fact, our results point at a fundamental institutional difference, between

Tuscany on the one side, and England and Holland on the other: the productivity gap between industry and

services on the one hand and agriculture on the other hand in Tuscany was much

larger than in England and Holland. Furthermore, in Tuscany

contrasts between city and countryside are exacerbated by the large income

streams from agriculture to the cities (and in particular Florence). This

increases the income of the urban elite – which spends it on the conspicuous

consumption that gives rise to the Renaissance – and depresses rural incomes.

These findings confirm an institutional

explanation of Tuscan economic decline first put forward, in pioneering works,

by Stephan Epstein, in the early 1990s, and later corroborated by several

studies on the basis of different sources (such as those by Van Bavel, Cohn, Alfani and

Ryckbosch, Alfani and Ammannati): Tuscany was characterized by high extractive

rates in favor of the elite of capital city, to the detriment of the subdued

cities and, most of all, of the countryside. This led to underdeveloped markets for

labor and capital in the countryside, which sharply contrasts with what we know

about Holland and England, where mobility of labor and capital was much higher.

In Tuscany, these blockades to market functioning in turn resulted into very

low productivity in agriculture, a high share of labor in agriculture and, arguably,

lower economic growth. The high extractive rate by the capital elite also

brought about a very high income per head in industry and above all in services,

as compared to agriculture: this may also explain why, in spite of a small

difference in per capita GDP, Tuscany boasted a much richer material culture

with respect to England and Holland, as testified by the florescence of the

arts in the capital city at that time: the surplus income was invested in

beauty.

The peculiarity of Tuscany’s institutional pattern (with respect also to

other Italian territories, such as Lombardy and Sicily) helps to understand the

limitation of GDP estimates based on the indirect approach, as are the series

available for pre-industrial Centre-North of Italy: these tend to be heavily

based on a few sources and for specific sectors and territories. In this case,

the real wages of the construction workers from Florence may not be a good

proxy of the entire urban sector, for a fragmented economy where labor

and capital were immobile as Tuscany was; let alone for the entire Centre-North

of Italy. Moreover, when it comes to international comparisons and long-run

historical series differences in purchasing power parities must be properly

considered, as well as their changes through time.

Our conclusions may be a useful result for other ‘fragmented’ economies

as well, and for historical estimates based on a few hypotheses over-extended

through time and space: cautiousness is warranted, and should always be

complemented by direct evidence when available. But we also point – very

indirectly – to the paradox that the beauty of the Renaissance, the unmatched

brilliance of its arts, was made possible by the highly uneven distribution of

wealth and income that in the long run undermined the vitality of Tuscan

economy and society.

Wolf-Fabian HUNGERLAND and Nikolaus WOLF.

The full paper in the EREH can be read here

We are used to distinguishing between the “first” and the

“second” globalization, separated not only by two world wars, but also by

changes in technology and institutions, and hence their basic economic logic. The

first globalization is typically described in terms of “classical” trade models

of comparative advantage, where countries trade to take advantage of their

differences. In contrast, the second globalization is largely described in

terms of “new” trade models based on monopolistic competition and firm

heterogeneity. Here, similar countries trade because they are all populated by

firms exploiting economies of scale and differences in productivity.

The similarities and differences between these two globalizations

are subject to a large and growing literature (Baldwin 2016, Jacks and Stürmer

2020). Given the rise in trade between very different countries like the USA

and China, Paul Krugman asked during his Nobel prize lecture of 2008: “is the

world becoming more classical?” (Krugman 2008). In a new paper (Hungerland and

Wolf, EREH forthcoming), we describe Germany’s foreign trade 1880-1913 with new

and very detailed evidence. To us, this evidence begs the question of how “classical”

has the world ever been in the first place? Put differently, to what extent can

“new” trade theory help us to understand the first globalization?

We have three main findings. First, and least

surprising, Germany got increasingly specialized in manufacturing, notably

chemicals, machinery and transport equipment. This is fully in line with

predictions of “classical” trade models, and Germany having a comparative

advantage in industries that use physical and human capital intensively. Second,

however, we find that nearly all growth in exports and most growth in imports took

place along the extensive margin, mostly driven by new products traded with old

trade partners. Third, we find that between 25-30% of trade at our finest level

of disaggregation is intra-industry trade, i.e. trade in the same product

category. The latter two findings imply that we cannot understand the first globalization

unless allowing for very substantial heterogeneity within countries and industries.

To create our data, we first digitalized all

historical statistics on the foreign trade of the German customs union and the

two major port cities Bremen and Hamburg that stayed outside of that customs

union before 1889. Our data covers all imports and exports from 1880 to 1913 of

all products, with all trade partners, captured in values and quantities. Next,

we reclassified all data to the SITC system, and used a quota method to merge

the Bremen and Hamburg data with that of the German customs union to create one

consistent dataset. Using the SITC, we can compare this to historical trade

data for other countries (e.g. Italy, see Federico and Wolf, 2012) and modern

trade data. In a related paper, Hungerland and Altmeppen (2021) provide details

on this and discuss, which revision of SITC is best suited to create

comparable, historical and long-run trade data.

Figure 1 shows the growth of imports and exports of

the German Empire, 1880-1913. This trade growth was much faster than GDP,

resulting in a rising openness ratio. Moreover, Germany was catching up to the

UK, to become the second largest trading nation in the world by 1913.

FIGURE 1

AGGREGATE IMPORTS, EXPORTS, TRADE BALANCE

|

In

1913-marks. Statistical items excluded. Source: Own calculations.

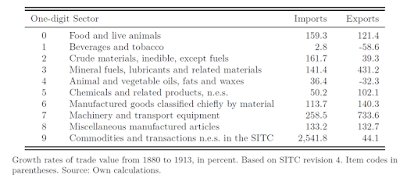

Table 1 is a first cut through the aggregate data: we see

how imports and exports grew between 1880 and 1913 at the level of 1-digit SITC

sectors. The pattern is roughly in line with “classical” trade models, where

exports of manufacturing products grow more rapidly than imports, while the

opposite holds for agricultural products and raw materials. However, the growth

of manufacturing exports is accompanied by very strong growth in manufacturing

imports, and Germany continues to export agricultural products and especially

raw materials (such as coal).

TABLE 1

SECTORAL TRADE GROWTH

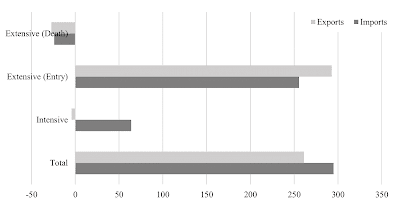

Our data allows us to dissect aggregate trade growth much further, down to the level of 5-digit SITC (the product-level) for each trade partner of Germany. The number of products traded increased from 334 in 1880 to 834 in 1913, while the number of trade partners grew from 34 (1880) to 86 (1913). Let us define each product-country combination as a variety. In 1880 we observe 971 import varieties and 1,482 export varieties. A generation later in 1913 we observe 10,145 import and 29,263 export varieties. Following Amiti and Freund (2010), we can decompose aggregate trade growth over all varieties into three margins. First, growth can occur along the intensive margin, where trade in existing varieties is expanding (“more of the same”). Second, there can be growth along the extensive margin, where new varieties enter (either old products are traded with new trade partners, new products traded with old trade partners, or new products with new trade partners). Finally, growth can occur along the extensive margin, where old varieties disappear. Figure 2 shows the relative contribution of each of these margins to Germany’s trade expansion before World War I.

FIGURE 2: MARGIN DECOMPOSITION, 1880-1913

|

| Margins in percent of total trade according to eq. 1. Source: own calculations. |

Clearly, the extensive margin dominates the picture.

Interestingly, this is true for imports and exports alike. In our paper, we

show that the extensive margin dominates growth in all types of trade,

manufacturing and non-manufacturing, and trade within and outside of Europe. Even

trade growth between Germany and the USA was dominated by the extensive margin.

Within the extensive margin, the most important element is the entry of new

products in trade with existing trade partners. Moreover, we show that this is

unlikely to be a statistical artefact stemming from an increasing level of

detail in the historical classification system. If we restrict our attention to

only those products and countries that were already recorded in the first year

of our sample (1880), the picture remains largely unchanged (although this

certainly underestimates the extensive margin).

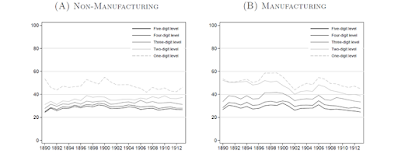

A related question is whether and to what extent there was intra-industry trade, hence exports and imports of the same products in a given year. In figure 3 we show, separately for non-manufacturing and manufacturing trade, what share of trade is intra-industry, varying the level of aggregation from sectors (1-digit SITC) to products (5-digit SITC).

FIGURE 3

INTRA-INDUSTRY TRADE

|

| Intra-industry trade in percent of total trade, Figure 3A: SITC sectors 0 to 4. Figure 3B: SITC sectors 5 to 8. Source: Own calculations. |

We find that even at the product-level, intra-industry trade accounts for between a quarter and a third of all trade, in manufacturing and non-manufacturing. Zooming into this more closely, we find that intra-industry trade was more prominent with rich economies—i.e. mostly with European trade partners.

Overall, our evidence suggests that simple “classical”

trade models that focus on differences between countries miss crucial aspects

of the first globalization. Once disaggregated trade data becomes available, we

see that most of the growth in imports and exports was due not to increase in

the value of trade in specific products between trade partners but growth in

the number of products and trade partners. Our new evidence for Germany is in

line with similar findings for Belgium before 1914 (Huberman et al., 2017) and

Japan before 1914 (Meissner and Tang, 2017, 2018). Such growth along the

extensive margin may have been driven by changes in trade costs due to improved

transportation technology, by rising incomes, or also reflect strategies to

differentiate products by branding and quality. But together with the evidence

on large-scale intra-industry trade this suggests that heterogeneity within

countries and industries should be systematically taken into account.

Yet, “classical” trade models are obviously not dead.

At a very broad level they seem to capture, how countries specialized before

1914 – after all, they were invented to capture exactly this. Germany did

specialize in manufacturing products, while agriculture in Germany and

elsewhere in Europe was increasingly exposed to import competition: the

“European grain invasion” (O’Rourke 1997) was very real. Farmers responded

either by giving up and leaving agriculture, lobbying for protection, or

shifting to different products (Suesse and Wolf 2020).

To us this suggests thinking about globalization along

the lines of a hybrid model such as Bernard et al. (2007) that combines

comparative advantages at the country-level with heterogeneity at the

firm-level. Doing so might have far-reaching implications for our

interpretation of the costs and benefits, the winners and losers, and hence for

the political economy of globalization. With more disaggregated trade data

available for more countries – hopefully in standardised and comparable form -,

this is opening the door for a new understanding of the history of

globalization.

References

Amiti, M. and C. Freund (2010), "The Anatomy of

China's Export Growth," NBER Chapters, in: China's Growing Role in World

Trade, pages 35-56, National Bureau of Economic Research, Inc.

Baldwin, Richard (2016), The Great Convergence. Information, Technology and the New

Globalization. The Belknap Press of Harvard University Press, Cambridge.

Bernard, Andrew B., Stephen J. Redding and Peter K.

Schott (2007), “Comparative Advantage and Heterogeneous Firms”, Review of Economic

Studies, 74, 31–66.

Federico, G. and Wolf, N. (2012). “A Long-run

Perspective on Comparative Advantage”, In: G. Toniolo (Ed.), The Oxford Handbook of the Italian Economy

since Unification, Oxford: Oxford University Press, chap. 12. 327–350.

Huberman, M., C. Meissner and K. Oosterlinck (2017),

“Technology and Geogrpahy in the Second Industrial Revolution: New Evidence

from the Margins of Trade“, The Journal of Economic History 77 (1),

39-88.

Hungerland, Wolf-Fabian and C. Altmeppen (2021), “What

is a product anyway? Applying the Standard International Trade Classification

(SITC) to historical data”, Historical Methods: A Journal of Quantitative

and Interdisciplinary History.

Hungerland, Wolf-Fabian and Nikolaus Wolf (2021), “The

Panopticon of Germany’s Foreign Trade, 1880-1913. New facts on the First Globalization”,

European Review of Economic History (forthcoming).

Jacks, D. and M.

Stuermer (2020), “What drives commodity price booms and busts?”, Energy Economics, 85, 104035.

Krugman, P. (2008), “The Increasing Returns Revolution

in Trade and Geography”, The Sveriges Riksbank Prize in Economic Sciences in

Memory of Alfred Nobel 2008, Prize Lecture.

Meissner, C., & Tang, J. (2017). “New goods and

markets versus more of the same: Japan's entry to world markets during the

first age of globalisation”, VOXEU.org, 16 June 2017.

Meissner, C., & Tang, J. (2018), “Upstart

Industrialization and Exports: Evidence from Japan, 1880–1910”, The Journal

of Economic History, 78(4), 1068-1102.

O’Rourke, K. H. (1997), “The European Grain Invasion,

1870-1913”, The Journal of Economic History, 57 (4), 775-801.

Suesse, M. and N. Wolf (2020), “Rural transformation,

inequality, and the origins of microfinance”,

Journal of

Development Economics, 143, 102429.

By Luigi Oddo (University of Genoa, Department of Political Science) and Andrea Zanini (University of Genoa, Department of Economics).

From

the second half of the 20th century, the role of urbanization in the

development process has become an extensively investigated topic. In standard

urbanization models, from the pioneering studies by Lewis (1954) on urban

pull factors, then passing on the great classics of the subject by de Vries

(1984) and Bairoch (1988), who stressed rural push factors, cities have

almost always been represented as a factor of economic development in the

pre-industrial world. Urbanization levels and city sizes have often been used

as empirical proxies for the level of income per capita (De Long and Shleifer

1993; Acemoglu et al. 2002, 2005; Malanima 2005; Maddison 2008; Dittmar 2011).

The

role of urbanization as a factor of economic growth has also been included in

the literature concerning Malthusian population theory. Clark

(2007) and Voigtländer and Voth (2009, 2013) suggested that high urbanization rates helped keep down fertility and

to drive up death rates, allowing living standards to rise, but through

purely Malthusian mechanisms. Overall, both urbanization models and Malthusian

population theory basically support the principle, even if through different

mechanisms, city growth

was a factor of economic advancement in the pre-industrial

world.

However,

in the last 20 years,

the idea that urbanization level is closely correlated with levels of income

and growth has started

to be questioned, especially in the literature concerning developing countries

(Fay and Opal 2000, Henderson et al. 2013, Gollin et al. 2016). The experience

of the Third

World in the second half of the 20th century clearly shows that

changes in income do not explain shifts in urbanization. Urbanization continues

even during periods of negative growth.

On

this basis, we aimed to shed light on the relationships between urbanization

and economic growth in the pre-industrial era, analyzing the case

of an Italian pre-unification state, the Republic of Genoa, from 1300 to 1800

with a novel dataset of cities and rural populations. Genoa was one of the most

powerful Italian maritime republics, probably exhibiting one of the highest degrees

of urbanization in Europe in the Late Middle Ages. However,

the history of the Republic of Genoa was described by cyclical Malthusian

stagnations, which were characterized by almost flat-lined growth at the

population level (Figure 1).

|

| Figure 1: urbanization (upper) and population (lower) of Genoa 1300-1800 |

The

coexistence of these contradictory elements raises the following question: is a

high degree of urbanization always a sign of economic advancement in the pre-industrial

world?

To

answer this question, our paper introduces elements of rural-urban migration

models within the Malthusian population theory to provide a different

perspective on the interactions between urbanization levels and demographic dynamics.

Focusing on the Republic of Genoa, this approach brings out that if high levels

of urbanization do not reflect substantial increasing productivity in

agriculture and growing urban labor demand, urbanization per se is not

sufficient to take-off from Malthusian stagnation. Therefore, the rise in

urbanization cannot match sustained economic growth. The natural consequence is

urbanization growth that follows a stop-and-go trend, where city populations

inflate and deflate cyclically. To describe this phenomenon, we coined the term

‘Malthusian urbanization’.

By Francisco J. Beltrán Tapia and (Norwegian University of Science and Technology; CEPR) and Francisco J. Marco-Gracia (University of Zaragoza; Instituto Agroalimentario de Aragón). Blog post based on the article with the same name published in the European Review of Economic History (here).

Many

pre-industrial societies regulated population size by resorting to infanticide

and the mortal neglect of unwanted infants and children (Langer 1972; Harris and Ross 1987; Hrdy 1999). These practices have traditionally

targeted girls in India, China and Japan, among other countries characterised

by strong patriarchal traditions that favour males (Das Gupta el al. 2003; Bhaskar and Gupta 2007; Drixler 2013). Women’s status in

historical Europe was definitely more advantageous than in other parts of the

world but Europe was not a gender-equal paradise and women were discriminated against in many dimensions (Szoltysek

et al. 2017; Carmichael and Rijpma 2017; Dilli et al. 2019). In this regard,

although the traditional narrative nonetheless defends that European families did

not neglect their female babies (Derosas and Tsuya

2010; Lynch 2011), several studies

suggest that female infanticide, as a means of controlling the size and sex

composition of their offspring, was more widespread that commonly thought, especially

in Southern Europe (Hanlon 2016; Beltrán Tapia and Raftakis 2021; Echavarri 2021).

By

relying on the parish records of all the population living in a rural Spanish region

between 1750 and 1950 (almost 60,000 individuals), this article evidences that discriminatory

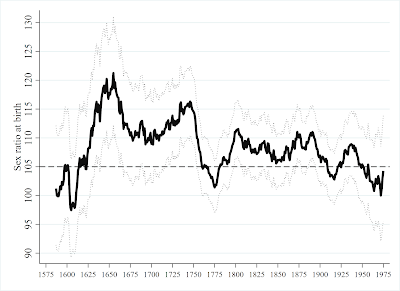

practices increased female mortality shortly after birth. Firstly, aggregate sex

ratios obtained from baptismal records were exceptionally high, at least until

the late 19th century (figure 1). Secondly, the individual-level

information shows that the probability of being male at baptism was

significantly higher when there were no previous male siblings alive, a feature

that could trigger discrimination in the presence of son preference. Likewise,

as evidenced by death registers, female survival chances during the first one

or two days of life were also negatively affected by this same feature, as well

as by the number of siblings alive. These findings seem to be concentrated at

higher parities and among landless and semi-landless families which were

subject to harsher economic conditions and therefore more likely to resort to

extreme decisions under difficult circumstances.

Figure 1. Sex ratios at

baptism, 1575-1975

Note: 25-year moving average. Dotted

lines represent the 95 per cent confidence interval. Source: AMHDB.

Crucially,

the fact that the results are robust to employing data from birth and death

registers rules out the possibility that under-registration explains this

pattern: although female misreporting would bias sex ratios at birth upwards,

it would have the opposite effect on mortality rates. Taken together, these

findings strongly support the idea that a significant fraction of female babies

were neglected or disposed away. These discriminatory patterns affecting female

mortality shortly after birth disappeared during the first decades of the 20th

century, as soon as the demographic transition and other economic, social and

cultural changes reduced general mortality rates and undermined the strong son

preference detected here.

The

mortal neglect of girls shortly after birth was probably a conscious family

decision that affected a number of families under certain circumstances. Apart

from the need to provide dowries for their daughters, the fact that there

existed less female waged labour opportunities also militated against girls.

The sources are though silent regarding how these girls went missing. There

were of course many ways of disposing of unwanted children and these crimes

were easy to commit and difficult to prove (starvation, dehydration,

strangulation, drugged to death, smothering, exposure to elements, etc. It is

also plausible that families could have not striven enough to keep them alive

especially during the crucial first hours of life. Given that there is

hardly any anecdotal evidence on female infanticide, our findings suggest that

some families disguised female infanticide or neglect as natural deaths.

The

evidence provided here shows that families especially targeted girls, but boys

could have undoubtedly fell victims to these practices as well. This article

therefore not only challenges the notion that there were no missing girls in

historical Europe, but also suggests that these families regulated the size and

sex composition of their offspring. These findings have important implications

for our understanding of the traditional demographic regime and the subsequent

transition to lower fertility and mortality rates because the relatively low

number of children raised by these families cannot be longer explained solely by

the use of different methods to reduce fertility either indirectly (delaying age

at marriage or celibacy) or directly (spacing or stopping). By increasing the

mortality of their unwanted children, these families also adopted a “death control”. The

gradual disappearance of these practices would therefore partly contribute to

explaining the decline in fertility and mortality that took place during the

demographic transition. Likewise, the fact that many of these deaths escaped

from birth and death registers also indicates that fertility and mortality

rates in these areas were higher than what it has been traditionally assumed.

Sara Torregrosa-Hetland

Oriol Sabaté

The World

Wars were associated with progressive tax policies in most Western countries.

Top marginal income tax rates increased to unprecedented levels, while other

fiscal instruments, such as excess profits taxes, were implemented during the

wars to meet the extraordinary revenue needs (Scheve and Stasavage, 2016).

In the

income tax, this leap in progressive reforms came along with the broadening of

the tax base, which brought for the first time low and middle incomes into the

tax (Brownlee, 1996; Broadberry and Howlett, 1998, 2005; Rockoff, 2012). This

fundamental transformation was the result of both regulatory changes, which

reduced exemption limits and personal deductions, and high levels of inflation,

which eroded the real value of these same exemption limits and deductions, pushing

incomes previously excluded from paying the tax into the fiscal net (even

though their real incomes did not increase).

Our

latest paper published in EREH (Torregrosa-Hetland and

Sabaté, 2021a) quantifies the role that inflation played in the

downward expansion of the tax during the World Wars. We first clarify and

estimate the ways in which inflation affects the distribution of income tax due

across different levels of income, and, second, calculate its effects on tax progressivity

and redistribution. Specifically, we analyze the income taxes of Sweden,

the United Kingdom and the United States, by comparing the actual operation of

the tax with alternative counterfactual scenarios of lower or no inflation

(here, as in the paper, we concentrate on our first counterfactual, defined by

the level of inflation over the five pre-war years). The exercise is based on

disaggregating the original tabulated tax data (following Blanchet et al.,

2017), and imputing income tax payments to the synthetic observations according

to the regulations in place (see also Torregrosa-Hetland and Sabaté, 2021b).

Inflation expanded the tax: more taxpayers, more

revenue

Our results

show that inflation was indeed a powerful mechanism for the downward expansion

of the tax. By the end of World War I, 75% of British taxpayers had been

incorporated into the fiscal net by excess inflation. This figure reached 68%

and 38% in Sweden and the United States respectively. The impact of inflation

by 1920 in Sweden was so extreme that these new taxpayers amounted to 28% of

the total tax units in the country (i.e., of the total number of potential tax

returns if everyone would have been required to file). During World War II,

nearly 4 million British taxpayers started paying the tax for no other reason

than nominal increases in their incomes (see Table 1).

Table 1. Additional taxpayers brought in by inflation

|

Country |

Year |

Scenario |

New taxpayers brought in by inflation |

||

|

Absolute number |

Percent of total taxpayers |

Percent of total tax units |

|||

|

Sweden |

1920 |

1 |

933,924 |

71% |

30% |

|

1920 |

2 |

876,513 |

68% |

28% |

|

|

1946 |

1 |

292,665 |

11% |

8% |

|

|

1946 |

2 |

166,053 |

6% |

4% |

|

|

United Kingdom |

1919 |

1 |

2,913,250 |

77% |

12% |

|

1919 |

2 |

2,840,603 |

75% |

12% |

|

|

1949 |

1 |

6,282,209 |

45% |

24% |

|

|

1949 |

2 |

4,013,889 |

29% |

15% |

|

|

United States |

1919 |

1 |

1,488,373 |

44% |

4% |

|

1919 |

2 |

1,300,997 |

38% |

3% |

|

|

1946 |

1 |

2,670,648 |

6% |

5% |

|

|

1946 |

2 |

1,484,428 |

4% |

3% |

|

Inflation

did not only bring new taxpayers into the tax, but also pushed existing

taxpayers into higher tax brackets (due to the erosion of the real value of

bracket limits and deductions). As a result, inflation was responsible for as

much as 80% of the income tax revenue in Sweden in 1920, and near 65% and 57%

in the United Kingdom and the United States in 1919 (see Table 2). Of this

additional “inflation revenue”, the majority was paid by existing taxpayers

that had been pushed into higher tax brackets (84% in Sweden by the end of World

War I, and above 90% in the United Kingdom and the United States; see Table 3).

New taxpayers entered massively into the tax during the two wars, but their

relatively low effective tax rates (particularly during World War I) made the

revenue impact more modest in absolute terms.

Table 2. Additional income tax revenue brought in by inflation

|

Country |

Year |

Scenario |

New tax revenue brought in by inflation |

|

|

Million current krs / £ / $ |

Percent of total income tax revenue |

|||

|

Sweden |

1920 |

1 |

145 |

82% |

|

1920 |

2 |

142 |

80% |

|

|

1946 |

1 |

588 |

44% |

|

|

1946 |

2 |

391 |

29% |

|

|

United Kingdom |

1919 |

1 |

210 |

67% |

|

1919 |

2 |

200 |

64% |

|

|

1949 |

1 |

822 |

67% |

|

|

1949 |

2 |

602 |

49% |

|

|

United States |

1919 |

1 |

880 |

63% |

|

1919 |

2 |

801 |

57% |

|

|

1946 |

1 |

7,629 |

41% |

|

|

1946 |

2 |

4,966 |

27% |

|

Table 3. Distribution of the additional revenue caused by inflation

between taxpayer groups

|

Country |

Year |

Scenario |

New taxpayers brought in by inflation |

Rest of taxpayers |

Top 10% of tax units |

Top 1% of tax units |

|

Sweden |

1920 |

1 |

17.3% |

82.7% |

80.6% |

52.3% |

|

1920 |

2 |

15.2% |

84.8% |

80.3% |

52.0% |

|

|

1946 |

1 |

3.9% |

96.1% |

57.0% |

27.3% |

|

|

1946 |

2 |

2.9% |

97.1% |

56.9% |

27.1% |

|

|

United Kingdom |

1919 |

1 |

8.0% |

92.0% |

97.8% |

76.6% |

|

1919 |

2 |

7.6% |

92.4% |

97.6% |

76.1% |

|

|

1949 |

1 |

17.3% |

82.7% |

66.7% |

33.5% |

|

|

1949 |

2 |

13.4% |

86.6% |

65.0% |

32.3% |

|

|

United States |

1919 |

1 |

8.0% |

92.0% |

99.9% |

80.6% |

|

1919 |

2 |

7.1% |

92.9% |

99.9% |

80.4% |

|

|

1946 |

1 |

0.7% |

99.3% |

55.0% |

31.0% |

|

|

1946 |

2 |

0.4% |

99.6% |

54.7% |

30.6% |

Inflation made the income tax less progressive, but

more redistributive

What was

the impact of these changes in the progressivity of the income tax? Since the

increases in tax burden were, in relative terms, more intense at the bottom of

the income distribution, inflation had a regressive effect. This was particularly

true in the United Kingdom during World War I. Figure 1 and 2 show the extent

to which low and middle incomes became subject to higher average effective tax

rates by the end of the wars due to inflation.

Figure 1.

Average effective tax rates under different inflation scenarios at the end of

WWI

Figure 2. Average effective tax rates under different inflation scenarios at the end of WWII

Interestingly,

though, the impact of inflation on redistribution was positive. While inflation

reduced the level of progressivity, it increased the size of a still

progressive tax, which in turn increased the amount of income that was placed

into the redistributive channel. For instance, the British income tax reduced

inequality by 5.11 Gini points in 1919, and no less than 28% of this effect was

caused by accumulated excess inflation since 1913. In this way, inflation was

one of the drivers of the transition from a ‘class tax’ into a ‘mass tax’: one

that obtained revenue from most of the population, forming a strong basis for

fiscal citizenship, and which became one of the major redistributive instruments

of the post-war era/for decades to come.

References

BLANCHET, T., FOURNIER, J., and PIKETTY, T. (2017):

Generalized Pareto Curves: Theory and Applications. WID.world Working Paper

Series 2017/3.

BROADBERRY, S. and HOWLETT, P. (1998): 'The United Kingdom: ‘Victory at all costs’',

in M. Harrison (Ed.), The Economics of

World War II: Six Great Powers in International Comparison. Cambridge:

Cambridge University Press, 43-80.

BROADBERRY, S. and HOWLETT, P. (2005): 'The

United Kingdom during World War I: business as usual?', in S. Broadberry and M.

Harrison (eds.) The Economics of World

War I, New York: Cambridge University Press, 206-234.

BROWNLEE, E. (1996): Federal Taxation in America: A History, New York: Cambridge

University Press.

ROCKOFF, H. (2012). America’s

Economic Way of War. War and the US Economy from the Spanish-American War to

the Persian Gulf War. Cambridge:

Cambridge University Press.

SCHEVE, K., and D. STASAVAGE (2016): Taxing

the Rich. A History of Fiscal Fairness in the United States and Europe.

Princeton University Press.

TORREGROSA-HETLAND, S., and SABATÉ, O. (2021a): 'Income tax progressivity and inflation during the World Wars', forthcoming in European Review

of Economic History.

TORREGROSA-HETLAND, S., and SABATÉ, O. (2021b): 'Income taxes and

redistribution in the early twentieth century', Lund Papers in Economic History:

General Issues; no. 224.